News

Stocks had their worst week in many years last week. The news doesn't look good.

February 16, 2022

Related Links

Is it written somewhere that we should all focus on the bad in everything or is this a particular ‘quality’ of the British? I was thinking about this recently and it led me to wonder if US stocks are higher relative to earnings because they are a more upbeat nation?

This is obviously a very difficult premise to prove, but it is an interesting hypothesis nonetheless.

Last week, stocks had their worst 5 days since March 2020 (the famous 1stlockdown). Yesterday, they opened even lower, and then they absolutely collapsed. It got to the point where we just couldn’t find a buyer.

There was panic in the equity market, stocks were dropping, but the odd thing was, there weren’t signs of panic anywhere else; risk off assets remained fairly measured. This is usually a good time to buy and hold, and weather current the storm, but the storm got worse.

Bond yields still weren’t moving, credit spreads still weren’t moving, in fact, very little else was moving anywhere. Even gold had no reaction. In short, what this means is that it wasn’t risk off, it wasn’t due to any problem with the economy, it was simply focused selling.

Everywhere we looked, on the back of the collapse, there were headlines about Russia, inflation, or imminent interest rate rises as market news and commentary looked for answers as to why this was happening. They were shouting about the panic, which was actually just fuelling more panic.

I think it would be nice if, from time to time, they just said we don’t know. Russia is escalating, which might be making a few investors nervous, fair enough. At this point, we would expect a reaction, but not like the one we saw.

Interest rate rises and inflation was news a few months ago, but that’s been and gone. If anything, the market might have overdone it. So, my guess is, they just didn’t know and so were saying anything, which seems to be more important than saying the right thing.

It really does seem to be the case that saying anything at all, right or wrong, is better than saying ‘we don’t know’. We get clients asking us about things they’ve heard on the news and how it’s obvious that stocks have dropped because of……….well……….whatever they happen to be saying on Bloomberg at the time.

This is when the markets dictate the narrative, and not the other way round. It’s a very common phrase in our world, but not one that is so well known outside it.

Commentators say bad things are happening if the market goes down, and good things are happening if the market goes up. That makes them look like they know what they’re talking about, but take it with a pinch of salt. It is very easy to do, and there is always something both good and bad happening in the world at the same time so they get to take their pick.

If they all actually knew which way the market was going to go, they certainly wouldn’t be working for a news channel.

24-hour news, and instant, constant reporting is almost certainly to blame for a lot of ‘fear’ in the market. It is very useful for staying on top of events as they unfold, but it can be very off-putting if you actually listen to their opinions.

Once the market drops, we get told why. It goes up, we get told why. But believe me, nobody can be sure what will happen tomorrow.

Yesterday we were told this by Morgan Stanley:

“Hunker down for a few more months,” as slowed earnings growth joins monetary policy uncertainty as primary market concerns.

The S&P could plunge another 10% with the “most speculative parts” of the market having been hit the hardest already, including names like Peloton being down 75% in six months.

BUT UBS TOLD US THIS:

In emailed comments on Monday, Frank Panayotou, managing director at UBS Private Wealth Management, said the dip in stock prices this year “seems overdone and represents a buying opportunity for long-term investors.”

He points out stocks have historically performed well in the months leading up to the Fed’s first rate hike, but he cautions markets will be more volatile than usual. “Investors need to be prepared for more volatility and overall more muted equity market returns than we have been accustomed to in recent years,” he said.

Two of the biggest investment banks in the world saying two very different things. Fine, it’s opinion. Generally speaking, people find the opinion they are looking for and go with that one. As a trader, we don’t have that luxury, because blaming someone else’s opinion won’t get us our money back.

So, what was the real reason for the sell-off and should we ‘buy the dip’ as UBS suggests, or is there more to come as Morgan Stanley suggest? Of course the answer is potentially either, or even both, one after the other, but let’s not sit on the fence.

We can only give our own opinion, and so here it is.

Let’s look at what we do know:

So, from this, here is a theory.

Many funds and almost every retail investor have been tech heavy since the summer after the virus struck. At that time, all we heard was ‘buy quality’; by this they meant, buy stay at home tech stocks with lots of money that the companies reinvest, rather than pay dividends. It’s hard to disappoint on the dividend front if you’ve never really paid them before and your investors don’t expect them.

So generally speaking, the investing world was way overweight growth stocks, and in particular, US tech. To prove that, all we have to do is look at some of the increases in share prices for 2021:

Netflix: +16%

Apple: +32%

Tesla: +42%

Microsoft: +51%

HP: +52%

Moderna: +62%

Just 5 stocks contributed over a third of the S&Ps total return in 2021 which means most of the money was going in one place, well, maybe between 5-10 places.

This does not sound like investors had diversified global equity portfolios. As we have said many times since the pandemic hit, these were the high return safe havens and the best places to store capital during this time: big tech with large balance sheets were safer than banks, and the vaccine producers had to do well, but only for the shorter term.

It seems obvious really, and it was. In fact it was so obvious, that literally anyone with a broking account was buying the same thing. I-phones across the world were being pressed: ‘Buy AAPL’ and ‘Buy TSLA’. That is how a bubble was formed. At the same time we said investors were going for safe haven stocks in 2020, we pointed out that this would inevitably lead to a tech bubble.

Until a vaccine was found, capital allocation in stay-at-home stocks made perfect sense. Maybe hold a little longer until the lockdowns eased but surely at that point, it was time to get out and diversify. BUT that never happened. Big tech kept going all through 2021.

Last week, we saw a taste of what could happen if asset allocation really started to take place. Or in this case, not so much ‘asset allocation’, as ‘equity sector reallocation’.

From an institutional point of view, overweight big tech now, just isn’t viable considering we’re coming out of the pandemic. They will still hold a portion for the long term because they have to, but some of the share prices trade more like crypto than stocks and funds can’t explain that kind of volatility to clients.

Just ask ARK, a fund which manages nearly $24 billion and is down 50% since the start of 2021.

Retail investors may have patted themselves on the back after last year, as they tend to buy, and then buy a little more, assuming that these shares will keep rising for ever, much like crypto does, or did. It might all rise again, but for now, they have just had a stark realisation: stocks do go down as well as up.

This shows how the same stocks shown above have fared so far in 2022:

Apple: -12%

Microsoft: -12%

HP: -13%

Tesla: -22%

Moderna: -33%

Netflix: -35%

Tesla has a p/e ratio of 111 times earnings. I can see only one reason for this: absolute madness. Retail investors around the world will buy things because Elon Musk tweets them. He can move crypto markets in an instant, and they love him for it.

Why sell off now?

The catalysts which set the collapse in motion, were the same ones we’ve been talking about for weeks, interest rate rises and a reduction of stimulus. But they weren’t enough. The escalating trouble with Russia seems to have turned the ripples into a tidal wave.

How to reallocate capital as a trader

The first thing to be done, is to sell the shares you don’t want. This was, and potentially still is, billions of dollars of shares in big tech. If you sell too many, computers will see the momentum build, and algos round the world will also start selling. This happened.

Then you have the retail investors who don’t really know what’s happening or why, but they don’t want to lose their money, so they start selling. This again, escalates. The snowball effect has begun.

Everyone is selling, and without a buyer, the fall is exaggerated and this inevitably starts to roll over into other sectors. Soon everything is falling.

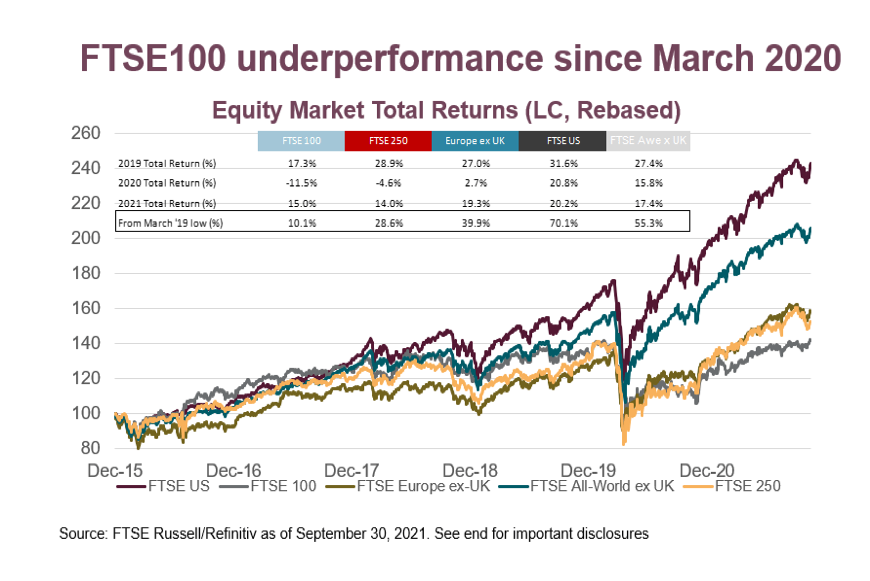

Even the FTSE dropped 6% and this is an index famous for its lack of tech.

Simply put, and it sounds silly, but when there are no buyers, stocks will fall. Growth stocks are volatile and their movement exaggerated. When a company like Tesla has a p/e ratio of 111, it could drop 50% and be entirely justified. I’m not saying it will, the appetite among young investors for the stock is remarkable, but it’s a frightening place to be for anyone who looks at the actual numbers.

What’s next?

We wish we had the answer, but what we can tell you, is the economy is stable, we are still coming out of the pandemic, and growth is looking very strong.

Marty Fridson, of Lehmann Livian Fridson agrees with our sentiment and commented on the relative calm of the bond market:

‘This seems to suggest that the inflation premium is growing, and higher discount rates are being applied [to stocks]. That is different from saying the economy is collapsing.

There doesn’t seem to be a concern about earnings, but rather about valuations. It’s not an economic issue that would cause [bonds’] default premium to rise’.

Of course we can’t make sense of extreme intraday volatility, because it is not required to make sense. There was an old trading joke on the floor that when asked why the market went down today, someone would respond ‘because there were more sellers than buyers’. Sometimes, this explanation will have to do.

We don’t feel this is a collapse for any real economic reason. No other assets moved in the same way to suggest a flight to safety. This was a sell-off in tech that sparked a reaction elsewhere. Big tech, is just too big.

Apple alone is worth as much as the entire FTSE100. Whatever happens in the US stock market, happens elsewhere.

We do feel the FTSE will come back and is a good place to be right now, but it will need buyers. When funds look for good value, that’s where they’ll find it, but it won’t get the fast money that makes indices jump; it will get sensible long-term investors, and that just isn’t any fun for most.

The current P/E ratio of the S&P is 27, for the FTSE it’s 15.

Summing up, then, it still looks like what we have is a relatively contained sell-off in equities, rather than a generalised flight from risk. Investors are acting jumpy, but not indiscriminately so. And within equities — to overgeneralise somewhat — the sell-off is focused on the kinds of things that have done well for much of the last decade, and especially well in the last two years.

Call it profit taking that escalated into something much more. Remain calm.

It’s hard to know what will happen next, but this could just be a minor revaluation that had a knock-on effect due to fear, panic, and the unknown.

Please do contact us if you have any questions. You might not have known you were looking for us, but you found us.

“TPP might just be about to revolutionise investment for the retail market.”

- London Stock Exchange 2020