Trading Guides

The single most important reason for this retail investor underperformance? Emotional human behavior.

October 27, 2021

Related Links

According to JPMorgan, over the past 20 years, the average investor reached an annual return of only 2.9%. As such, they significantly underperformed the general market as the S&P 500 yielded an annual 7.5% return during this time frame.

The single most important reason for this retail investor underperformance? Emotional human behavior.

The average investor is getting influenced heavily by media headlines, stock prices movements and behavior from other investors.

Today, we reached an extremely bullish stock market environment. Last earnings season has been one of the greatest in stock market history. The S&P 500 EPS rose by 94.5% YoY and 86.1% of its constituents beat analyst estimates.

As a consequence of this bullish environment, analysts are significantly raising their estimates for the next quarters. They now expect EPS to rise sharply to $217.96 by the end of 2022, which is a significant recovery from the pre-pandemic high of $157.12. Such a recovery looks to be optimistic as it took 7-12 years in the past economic cycles to achieve this:

Will earnings really continue this very strong recovery over the coming quarters or are analysts perhaps getting too greedy with their assumptions?

It wouldn't be the first time if they were too greedy. During the dot-com bubble for example, they were caught by their emotions as well. The '90s was an abnormally strong decade in terms of earnings growth for the S&P 500. As such, analysts totally forgot that downward cycles exist as well. They increased their annual EPS growth guidance to a staggering 15% for the five years following 2000. According to them, this high growth rate justified the record P/E multiples stocks were trading at and many investors got tricked into that story.

What happened afterwards? The economy didn't boom, it fell into a recession which took 3 years to recover from. Earnings in 2003 were almost 50% lower than what analysts had been predicting in 2000.

As markets were priced to analyst expectations instead of taking into account a possible downturn, the S&P 500 crashed and took 7 years to recover.

Let's get back to today... The P/E of the S&P 500 currently stands at 25.4x, which is extremely high compared to historical levels. This gets justified by the common belief that earnings will continue rising significantly. As such, the ratio would fall to an acceptable 20.7x by the end of 2022.

Now ask yourself how likely it is that earnings growth will continue to grow at higher levels than the historical average over the coming quarters.

Interest rates are already at 0%. The money printer is running out of paper. Federal debt levels are hitting their ceilings. Pent-up demand and stimuli cheques already led to record-high consumer spending over the past quarters.

Maybe, just maybe, analysts are being too greedy with their assumptions? Maybe the recent economic recovery is unsustainable and set to cool down? Maybe my assumptions (grey line) are much more likely than what the market is predicting (red line)? If so, the market is trading at a fwd 2022 P/E of 23.6x, which is really expensive.

I'm not sure this will happen, nobody is. But it sure as hell is a probability.

This greediness also gets reflected in the charts. As you can see in the chart below, a bull market can be split into four cycles. Strong growth, bear trap, media attention and greed.

Interestingly, the 2013-2021 bull market is playing out almost identically as the 1994-2000 bull market. At this moment, the Nasdaq Index (QQQ) looks to be ready to start the last extreme greed phase. The media is approaching the recent rally as "the new normal" and investors are FOMO buying heavily because stocks "can only go up". As such, it is likely that the Nasdaq will rise close to $20,000 in the last months of 2021.

As a long-term investor, it is extremely important to understand these dynamics. You will probably feel the urge to go all-in in risky assets as well. However, getting greedy during this phase could be a major threat for your long term returns as it will likely be followed by a major bear market.

Human behavior makes it extremely challenging to not get distracted by market sentiment. If you can keep an objective view on markets, it will benefit your returns drastically.

In short, rule #1 says that your decisions should never be led by emotions and that you should keep focusing on underlying fundamentals. As the market is getting greedy today and valuations reach extreme levels it implies that you should start selling stocks and hold a lot of cash, right?

Not really... You know, a wise man once said the following:

It's a market of stocks, not a stock market.

I'm not entirely sure who came up with it. But it must be a wise man, for sure.

What does it mean? Look, many retail investors buy/sell stocks based on how the outlook for the general market looks like. If they don't trust the markets, they will be reluctant to invest, no matter what.

That's not a great way of looking at markets. There are almost 4,000 stocks available and there will always be interesting investment opportunities to generate great returns, no matter how the market evolves.

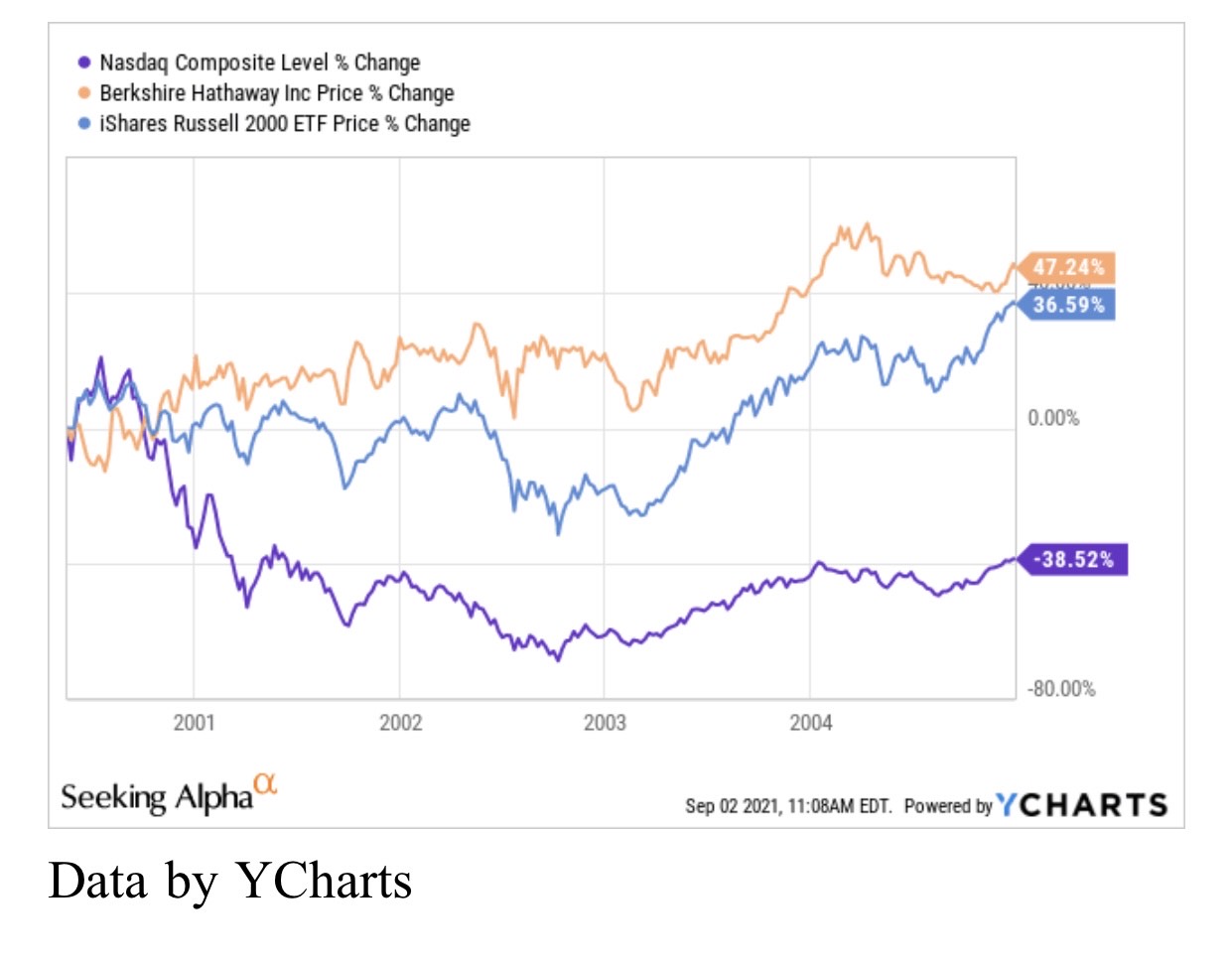

In a generally overvalued market it gets increasingly challenging to find undervalued stocks, but certainly not impossible. Ask Warren Buffett. In 2000, the most overvalued stock market in history, his investment vehicle Berkshire Hathaway (BRK.A) (BRK.B) kept buying high-quality, undervalued assets. His dedication paid off with an impressive return of 47% five years after the dot-com peak compared to -39% for the Nasdaq index.

The Russell 2000 (IWM), an index reflecting US small caps, was very attractive during the dot-com bubble as well, trading at a P/E of 16x (vs 24x for large caps) going into 2000. Those who invested in this undervalued asset class during the bubble also generated very solid returns. Those who were able to pick out the greatest small caps were a lot happier than those who got tricked into overhyped tech stocks, I can imagine.

So what should you do today? I would suggest re-evaluating all your portfolio holdings. Weigh their valuation compared to earnings 3 years from now, when Covid-19 disruptions (stimuli, pent-up demand, etc.) are gone. Be conservative with your assumptions. If a stock is significantly overvalued compared to those assumptions, don't be greedy and sell out the position.

A great example is Apple Inc. (AAPL), one of the most popular stocks this year. As a consequence of its very strong financials (revenue grew 36.4% last quarter), its P/E ratio more than doubled over the past two years to 30x. It is important to understand that its recent growth primarily accelerated due to unsustainable drivers such as the several rounds of stimuli cheques. Once this fades away, Apple's growth is likely to fall back to single digits (or might even go negative in the short term) and returns would be very weak going forward.

Don't keep all that freed up capital in cash, especially in the current inflationary environment. There are still opportunities to re-invest that money.

At The Portfolio Platform the traders we recruit are tasked with out performing the market regardless of the climate. Similar to 'stock bulls' they will buy individual equities and the Indices, but unlike many bulls- they're not afraid to go flat. They will also 'short sell' the markets when the opportunity presents itself, as well as initiate what we would term 'spreads' where they're buying one market (FTSE for example) whilst selling another (Nasdaq).

There is a reason the average trader on TPP achieved over 58% in 2020, and look on course to post a similar return in 2021. The traders and trading teams we have recruited are world class, and they take advantage of market opportunities. Our traders aim to achieve 2-4 times what the market produces on a yearly basis.

They won't always be right, there will be months when they underperform, but quarter on quarter and year on year- we would expect they'll deliver. Stock markets do seem over priced currently, and it's easy to have a fear of missing out, but be careful, and remain cautious. The markets can often surprise you.

If you would like to find out more about how The Portfolio Platform could benefit your portfolio regardless of the market climate- don't hesitate to schedule a call here.

“TPP might just be about to revolutionise investment for the retail market.”

- London Stock Exchange 2020